This week, we’re looking at one of my ‘favorite’ biases, in that it’s one that once you know, it can be quite comical to spot it in others (and yourself, if you still fall for it, from time to time). From Wikipedia: the overconfidence effect “is a well-established bias in which someone’s subjective confidence in their judgments is reliably greater than their objective accuracy, especially when confidence is relatively high.” That’s a bit jargon-y, so let me illustrate with a simple example.

This week, we’re looking at one of my ‘favorite’ biases, in that it’s one that once you know, it can be quite comical to spot it in others (and yourself, if you still fall for it, from time to time). From Wikipedia: the overconfidence effect “is a well-established bias in which someone’s subjective confidence in their judgments is reliably greater than their objective accuracy, especially when confidence is relatively high.” That’s a bit jargon-y, so let me illustrate with a simple example.

In fact, this example comes from a lecture I heard about negotiation and talked about in one of my previous posts. In case you were wondering, the lecture comes from Professor Margaret Neale at Stanford. It was a brilliant! There was so much information packed into the lecture. I remember listening to it a few different times and still pulling out nuggets of wisdom. Anyway, I digress. The example that Prof. Neale uses is particularly on point for illustrating the overconfidence effect.

She has an empty pop bottle filled with paper clips (but not to the top). She says to the crowd that she wants them to guess how many paper clips are in the bottle. She walks up and down the aisles, so they can get a closer look, too. She instructs the crowd to write down their answer. Then, she asks them to write down a range where they could be 100% (she may say 99%, I don’t remember) sure that the number of paper clips fell in the range. Essentially, she was asking for a confidence interval. I think she also told them that she was sure there weren’t more than 1,000,000 paper clips in there. After some time, she then tells the audience how many were in there. She asks if anyone got it right (no one raises their hand).  She then says something to the effect of, “For how many of you did the number of paper clips fall within the range?” There may have been about 35% of the room who raised their hand. 35%! She exclaims that this is terrible given that all of these people were 100% (or 99%) sure that the number would fall in the range. In fact, she said that in a room that size, there should have only been a handful of people who’s range wasn’t met (if the 99% figure was being used, rather than 100%). Prof. Neale then goes on to explain that this is the overconfidence effect. The audience was being asked to make an estimate of something about which they knew nothing, and then asked to rate their confidence. Knowing that they knew nothing about the topic, it would have been logical for the audience to have a large confidence interval (between 10 paper clips and 20,000 paper clips) — or even bigger!

She then says something to the effect of, “For how many of you did the number of paper clips fall within the range?” There may have been about 35% of the room who raised their hand. 35%! She exclaims that this is terrible given that all of these people were 100% (or 99%) sure that the number would fall in the range. In fact, she said that in a room that size, there should have only been a handful of people who’s range wasn’t met (if the 99% figure was being used, rather than 100%). Prof. Neale then goes on to explain that this is the overconfidence effect. The audience was being asked to make an estimate of something about which they knew nothing, and then asked to rate their confidence. Knowing that they knew nothing about the topic, it would have been logical for the audience to have a large confidence interval (between 10 paper clips and 20,000 paper clips) — or even bigger!

This happens in more ways than just simply estimating the number of paper clips in a bottle. We also see this with investors. When asked, fund manager typically report having performed above-average service. In fact, 74% report having delivered above-average service, while the remaining 26% report having rendered average service.

Another place that we see the overconfidence effect show up is with the planning fallacy: “Oh yeah, I can finish that in two weeks…”

Ways for Avoiding the Overconfidence Effect

1) Know what you know (and don’t know)

The fastest way to slip into the trap of the overconfidence effect is to start making “confident” predictions about things that you don’t know about. Guessing the number of paper clips in a bottle is something that most of us have little to no expertise in. So, list a large confidence interval. If you have no experience in managing a project, it might be in your best interest not to make a prediction about how long it will take to complete the project (planning fallacy).

2) Is this person really an expert?

Sometimes, you’ll hear someone displaying a level of confidence in a given situation that makes you think they know what they’re talking about. As a result, it might bias you into believing what they are saying. It’s important to know if this person is an expert in this field, or if maybe they’re succumbing to the overconfidence effect.

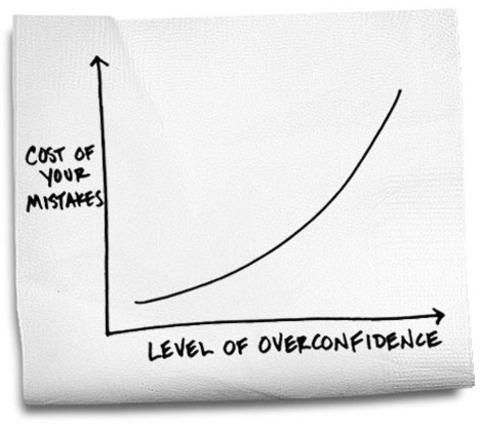

From Scott Plous‘ book called The Psychology of Judgment and Decision Making: “Overconfidence has been called the most ‘pervasive and potentially catastrophic’ of all the cognitive biases to which human beings fall victim. It has been blamed for lawsuits, strikes, wars, and stock market bubbles and crashes.”

If you liked this post, you might like one of the other posts in this series: